Key market movements

Global equities delivered another solid month in June, adding 4.4% in NZD‑unhedged terms (however ‑0.1% in NZD‑hedged terms as the New Zealand dollar weakened through the month). Market performance was supported by strength in AI‑related shares following robust results from memory‑chip manufacturers, alongside improving sentiment as tensions in the Middle East eased.

The New Zealand market extended its recent gains, with the S&P/NZX 50 Gross Index (including imputation credits) returning 2.9% over the month, driven by secular growth companies which benefited from falling long-term yields. Australian equities were softer, with the S&P/ASX 200 Index up 0.7% in Australian dollar terms and 2.2% in New Zealand dollar terms.

Fixed income returns were positive again for the month, with the Bloomberg NZ Bond Composite Index returning 1.2% and the Bloomberg Global Aggregate Bond Index (hedged to NZD) advancing 0.3%, as falling oil prices and easing geopolitical risks helped lower inflation concerns.

Key developments

Headline inflation risks have receded with the recent decline in energy prices, leaving underlying inflation to be increasingly determined by demand conditions. Oil prices dropped more than 20% in June to be almost 40% lower than their late-April highs and close to pre-Iran conflict levels. The signing of a US-Iran interim peace deal in the middle of June has allowed for a reopening of the Strait of Hormuz and an easing of supply constraints. At the same time, underlying inflation pressures may be reducing. In the US, investment continues to be supported by structurally strong spending in technology. Household consumption, however, may be losing momentum and the labour market is cooling.

The Fed left its policy rate unchanged at 3.50%–3.75%, as expected, but delivered a more hawkish signal through its updated projections and a shift in communication under new Chair Kevin Warsh. The Summary of Economic Projections showed a split committee, with roughly half anticipating further hikes and others expecting rates to remain unchanged, pushing median rate forecasts higher despite the long-run estimate remaining stable. Warsh removed forward guidance, emphasised price stability over employment, and signalled a preference for markets to respond directly to incoming data rather than Fed messaging, raising the likelihood of greater short-term interest rate volatility.

In Australia, the transmission of restrictive policy into activity has become more evident. Weaker household spending, softer housing market dynamics and limited employment growth have reinforced the view that policy is already restrictive. Inflation data during the month were mixed, with softer headline outcomes offset by persistent core measures, leaving the Reserve Bank of Australia (RBA) biased to retain optionality. The key constraint is credibility: having responded late to the prior inflation shock, the RBA appears reluctant to suggest the job is done until there is clearer evidence of a sustained disinflationary trend. At the same time, slowing growth is reducing the likelihood that further tightening will be required.

The Bank for International Settlements (BIS) Annual Economic Report commented on the financial stability risks that arise from near-record high public debt across the developed world, with the US Treasury Market also increasingly being funded by hedge funds using repo trades to buy Treasuries with a high degree of leverage. This part of the market is stable at present, but the BIS note the increased scope for volatility that could occur under stress. Growing fiscal concerns remain a medium-term risk unless governments in a handful of large economies can get on top of high fiscal deficits.

In New Zealand, the data during June pointed to a gradual improvement in forward-looking activity alongside ongoing spare capacity. Business surveys showed a lift in confidence and planned investment, but this remained inconsistent with realised activity, which is still soft. Inflation pressures moderated slightly, with declines in pricing intentions and a fall in short-term inflation expectations, but measures of non-tradable inflation remain elevated. The divergence between improving sentiment and weak current conditions suggests that the recovery is likely conditional on a continued easing in inflation pressures that allows the Reserve Bank of New Zealand to keep the Official Cash Rate below neutral (c.3.00–3.25%) for some time.

What to watch

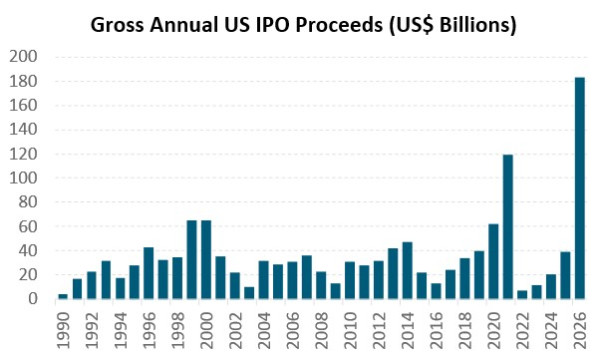

The chart below shows annual US IPO volumes from 1990 to present. Two things stand out. The first is how uneven the cycle has been: the 2021 boom was followed almost immediately by one of the deepest droughts on record, with 2022 and 2023 producing a fraction of that volume. The second is what is happening now. With half the year still to run, 2026 volumes have already surpassed the previous full-year record, driven largely by the SpaceX listing. Both OpenAI and Anthropic have also joined the sprint to market, with each reported to be aiming to raise around US$60 billion, although with no confirmed timing as of yet.

Source: Jay R. Ritter, University of Florida. Bloomberg.

Market outlook and positioning

The macro backdrop shifted materially through June, with the US-Iran ceasefire and the prospect of a more durable peace framework reducing the tail risk of a prolonged energy shock. Lower and more stable oil prices flowed through into inflation expectations, and long-term bond yields fell back toward levels that prevailed before hostilities began. There is now a reasonable prospect that inflation pressures will continue to ease and that central banks will not need to tighten as much as had been feared, though markets remain sensitive to any renewed disruption to shipping or energy supply.

The reduced inflation risk restores optionality for central banks. In New Zealand, the projected OCR peak has been revised lower toward a 3% terminal rate. That is a meaningful positive for interest rate sensitive sectors of our share market, including utilities and listed property. In the United States, the new Federal Reserve Chair, Kevin Warsh, inherits a Fed Funds Rate range of 3.50–3.75% and therefore has more room to manoeuvre; if inflation has indeed peaked, staying on hold remains a credible option.

Even with central banks under less pressure, the next test for markets is the second quarter earnings season. Corporate earnings growth has underpinned equities through 2026, and the bar is high as US heavyweights begin to report. Consensus expects year-on-year S&P 500 earnings growth of 23% on revenue growth of 12%, which would mark the seventh consecutive quarter of double-digit earnings growth. Artificial intelligence investment is likely to remain a powerful structural driver, though leadership may broaden beyond technology. June perhaps saw the beginning of this shift, as greater volatility among AI beneficiaries prompted investors to question returns on committed capital and rotate into previously oversold areas, including healthcare.

Regional divergence remains a feature of the outlook. The New Zealand share market is weighted toward defensive growth and secular growth companies, which have historically performed well in periods of disinflation. The Australian share market may see a more mixed period, as expectations reset for a slower domestic economy. Locally, the New Zealand economy remains sluggish but has proven more resilient than feared, with the ANZ Business Opinion confidence survey lifting sharply in June and inflation indicators easing.

Although risks remain, including further geopolitical developments, trade policy uncertainty and the potential for inflationary pressures to re-emerge, the broader investment backdrop has improved. Lower energy prices, resilient corporate fundamentals and expectations of gradually easing monetary policy provide a more constructive environment for long-term investors. Economic growth has proven more resilient than many anticipated, but earnings expectations have become more elevated, placing greater emphasis on the delivery of a strong corporate earnings season.

Within equity growth funds our strategy remains to be patient, position for a range of scenarios and to be selective, focusing on quality growth. We continue to focus on companies delivering earnings per share growth, particularly where that earnings growth has the potential to be higher and last for longer than consensus expectations allow for. We continue to see the secular tailwinds of digitisation, disruption, de-carbonisation and demographic changes as supporting company earnings. Our growth funds are overweight healthcare, predominantly via NZ retirement village investments where returns are expected to improve as supply and demand conditions stabilise and operational efficiency improves, as well as Australian pharmaceutical and diagnostics businesses with world-class products and services supporting long-term growth. The funds are also overweight select financials (where Challenger may benefit from improved capital efficiency, Infratil from data centre growth, and Macquarie from stronger transaction activity). We are underweight utilities, communication services and real estate, where valuation multiples remain full relative to modest earnings growth prospects.

In fixed interest, the decline in market yields that has occurred since the Middle East tensions diminished has taken the market closer to fair value. This has prompted us to reduce duration in portfolios back towards neutral levels. In longer-dated bond funds we are underweight in the 10 year and longer maturities, as the NZ market looks expensive and in global markets we perceive a skew of risks towards higher yields over the next few months.

In the Income Fund, we have lifted equity allocation from moderately underweight back closer to neutral, with the addition of exposure to global equities through Acadian Global Equities. Fixed interest strategy is in line with the fixed interest funds, with a reduction in duration, while we retain an overweight position in the New Zealand Dollar versus the Australian Dollar.

In multi-asset funds, we are overweight global equities and underweight Australasian equities on relative earnings prospects. We feel global equities should outperform Australasian equities given the US (which makes up almost 70% of the MSCI ACWI) has much better economic momentum. We are overweight in domestic fixed income, with market pricing of the OCR to reach 3.4% inconsistent in our view with the spare capacity in the economy. We remain underweight global fixed income where there is greater fundamental support for higher yields. We remain overweight the NZD as it continues to screen as undervalued based on our short-term model. However, we recognise that the currency has been trading in a range whilst the conditions to move towards fair value have not materialised, and so we remain active with our positioning as the currency moves around within this range.

IMPORTANT NOTICE AND DISCLAIMER

This publication is provided for general information purposes only. The information provided is not intended to be financial advice. The information provided is given in good faith and has been prepared from sources believed to be accurate and complete as at the date of issue, but such information may be subject to change. Past performance is not indicative of future results and no representation is made regarding future performance of the Funds. No person guarantees the performance of any funds managed by Harbour Asset Management Limited.

Harbour Asset Management Limited (Harbour) is the issuer of the Harbour Investment Funds. A copy of the Product Disclosure Statement is available at https://www.harbourasset.co.nz/our-funds/investor-documents/ Harbour is also the issuer of Hunter Investment Funds (Hunter). A copy of the relevant Product Disclosure Statement is available at https://hunterinvestments.co.nz/resources/.

Please find our quarterly Fund updates, which contain returns and total fees during the previous year on those Harbour and Hunter websites. Harbour also manages wholesale unit trusts. To invest as a wholesale investor, investors must fit the criteria as set out in the Financial Markets Conduct Act 2013.