Key market movements

• Global equities fell sharply in March, with the MSCI All Country World Index (ACWI) declining 2.4% in unhedged New Zealand dollar terms. Hedged investors experienced a more pronounced decline, with the ACWI falling 6.6% in hedged NZD terms, as the New Zealand dollar weakened over the month.

• Australasian equities sold off materially in March. The S&P/NZX 50 Gross Index (including imputation credits) fell 5.8%, reflecting broad-based weakness across the local market. Australian equities also declined sharply, with the S&P/ASX 200 Index down 7.1% in Australian dollar terms, or 6.1% for New Zealand dollar investors.

• Fixed income returns were also negative in March, with the Bloomberg NZ Bond Composite Index returning -1.7% and the Bloomberg Global Aggregate Bond Index (hedged to NZD) declining 2.0% for the month, as rising yields weighed on bond prices across both domestic and global markets.

Key developments

The Iran war has lifted global energy prices sharply, shifting the balance of risks toward higher near‑term inflation and tighter monetary policy. The shock is also a drag on growth, but central banks are signalling that inflation risks may need to be prioritised to keep inflation expectations anchored. Shipping through the Strait of Hormuz remains severely impaired for a large group of countries, energy flows are recovering only gradually, and crude oil prices have moved into the US$100–120 per barrel range. Freight, insurance and logistics frictions remain elevated, reinforcing higher costs across oil, petrochemicals and energy‑intensive materials.

Central bank responses have reflected this inflation–growth trade‑off. The Federal Reserve held policy at 3.75% and explicitly acknowledged that higher energy prices increase inflation risks. The European Central Bank held at 2.15% and emphasised its readiness to act should inflation expectations become unanchored. The Bank of Japan held at 0.75% while monitoring higher import costs. Australia stood out for tightening, with the RBA lifting rates by 25bp to 4.10% on a narrow 5–4 vote, explicitly balancing persistent inflation pressure against the likely growth hit from higher oil prices. Market pricing of rate hikes in most economies over the next 12 months is consistent with central banks prioritising inflation over growth.

Beyond the immediate inflation impulse, the energy disruption is already acting as a catalyst for structural adjustment. Elevated and more volatile energy prices are accelerating policy and capital allocation toward energy security, renewables, electrification and supply‑chain resilience. Unlike earlier energy shocks, viable substitution pathways now exist across much of the industrial and consumer economy, limiting the risk that higher prices translate mechanically into demand destruction. This supports a view that the medium‑term growth impact is more likely to be redistributive than contractionary, with pressure concentrated in energy‑dependent regions and sectors.

In New Zealand, the macro focus has shifted toward the same inflation‑growth tension, but from a weaker starting point for activity. The RBNZ laid out its framework that looks through temporary fuel price spikes while responding to any persistence in inflation, and it acknowledged softer growth momentum. The early economic impact has been visible through tourism, with international visitor cancellations linked to flight disruptions. Forward indicators softened, with the ANZ Business Outlook showing expected own activity easing and construction identified as the weakest sector.

Large amounts of spare domestic economic capacity argue against a sustained inflation overshoot, but they do not prevent a near‑term lift in headline inflation. An unemployment rate of 5.4%, for example, suggests meaningful economic slack that should limit second‑round effects. The key risk is persistence. Scenario analysis suggests that a disruption lasting several months could lift CPI materially while reducing GDP, testing the RBNZ’s ability to look through the inflationary effect.

Source: Bloomberg

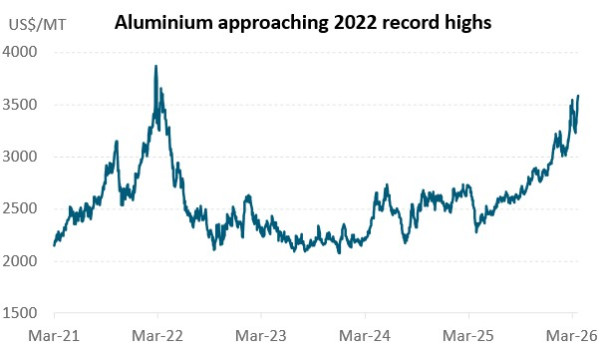

London Metal Exchange aluminium futures surged as much as 6% on the first day of trading after Iranian drone and missile strikes confirmed significant damage to two of the world's largest smelters, Emirates Global Aluminium in Abu Dhabi and Aluminium Bahrain. The Middle East accounts for around 9% of global aluminium production, but the impact is being amplified by already depleted inventories, leaving the market with little capacity to absorb further shocks. Even before becoming a direct target, Gulf smelters had been running short of key inputs following the closure of the Strait of Hormuz, with production cuts looming. The strikes raise the prospect of sustained supply disruption well beyond any reopening of the strait, with record prices a real possibility and meaningful implications for inflation, input costs, and materials-exposed sectors globally.

For New Zealand, the picture is more nuanced. NZAS at Tiwai Point in Southland produces aluminium using renewable hydroelectricity, giving it one of the lowest carbon footprints of any smelter in the world, with around 90% of its output exported. The smelter produces more than 335,000 tonnes annually, generating around $600 million in export earnings and contributing approximately $406 million to the Southland economy each year. Unlike Gulf producers, Tiwai Point is insulated from the direct supply disruption and, as a low-carbon producer, is well placed to attract a premium in a market increasingly focused on sustainable sourcing. A sustained period of elevated aluminium prices would represent a meaningful tailwind for NZ export income and, at the margin, a modest positive for the NZD.

Market outlook and positioning

The global economy is navigating three intersecting pressures: artificial intelligence disruption, protectionist trade policy, and geoeconomic fragmentation. Growth proved resilient through 2025, but fading tailwinds, higher energy costs and inconsistent policy direction have created a more divergent regional outlook. The United States may sustain reasonable momentum, China could prove a quiet outperformer, and parts of Asia-Pacific face the sharper edge of energy cost pressure. Deglobalisation and government industrial policy will produce winners and losers across sectors. Macro volatility remains well short of the extremes of the 1970s and 1980s energy crisis period, and global inflation expectations remain broadly anchored. World GDP growth may ease below its recent 3% run rate but is likely to remain in positive territory.

Higher starting bond yields provide a more useful anchor for well-diversified portfolio returns than was available through the low-rate era. Disruption and transition have always been constant features of investing, from the oil shocks of the 1970s through to the internet boom of the 1990s. History reinforces that staying invested and diversified remains the appropriate response to current uncertainty.

In New Zealand, we expect domestic recovery to continue, though at a measured pace. Company earnings per share have begun to lift, with several businesses entering an upgrade cycle, though the rate of improvement is likely to extend further out than initially anticipated. We see the Reserve Bank of New Zealand on hold for now, with low rates continuing to underpin economic activity.

AI disruption remains an ongoing influence on the macro backdrop, potentially contributing to higher rates of productivity and lower inflation pressure over the medium term. As AI increasingly performs cognitive, administrative and analytical tasks, value shifts away from labour‑intensive and process‑heavy models toward scale, data ownership and integration. The adjustment has already been evident across legal services, insurance and parts of the software ecosystem, where faster price discovery and margin pressure coexist with rising returns to scale for firms with clean proprietary data or regulated platforms.

Tighter financial conditions continue to emerge through private credit channels. While we do not view private credit stress in isolation as a systemic risk, evidence of redemption pressure for private credit funds highlights the interaction between higher funding costs, energy exposure and AI‑driven business model adjustment. Higher credit spreads, particularly in sectors exposed to these forces, act as an additional tightening mechanism even in the absence of outright credit events.

In fixed interest portfolios, due to the uncertainty that exists around both near and medium term outcomes in the Middle East, we are being cautious about active positions that are subject to favourable outcomes. However, we did add to exposure in NZ 1 - 3 year bonds when yields had risen well beyond levels that are consistent with a wait-and-see approach from the RBNZ. In the near term our judgement is that this trade has an attractive risk/return profile. Similarly, we prefer to be underweight long-dated bonds, as New Zealand, along with many other countries, shares a structural fiscal challenge. The outlook for government deficits also looks particularly problematic in the United States, which is relevant given the leading role it plays in a global context.

Beyond these themes, we continue to hold inflation-indexed bonds, which have been the strongest performer in March, generating significant added value in the portfolio. We have taken profit on a small amount of the position, while adding to holdings of 3 and 8 year bonds issued by the Local Government Funding Authority (LGFA). LGFA were the weakest part of the NZ market last month and are now nearer to fair value. The market volatility is also providing a degree of mispricing across some securities, so there are opportunities here that have appealing risk characteristics that are independent of the Middle East situation.

In the Income Fund we have continued to hold a hedge on global equity position, with overall equity exposure modestly below neutral. The defensive, income-generating equity holdings have fared very well through March. Within the fixed income securities, we have a 7.5% weight to inflation-indexed bonds and with the duration of fixed interest holdings averaging 3 years, sensitivity to rising bond yields is not high.

In multi-asset funds, early in the month we took our equity positioning to neutral. Towards the end of March, we approached levels that looked attractive to us to re-enter, but feel the recent rally has downside risk, and so we wait for a more attractive entry point again. We feel that global equities will likely be a better place to take risk, relative to the local markets, given our view that New Zealand will be impacted more than the US by the energy crisis. We are overweight in domestic fixed income, with continued pricing of hikes inconsistent in our view with the spare capacity in the economy. We remain underweight global fixed income where there is greater fundamental support for higher yields. We remain overweight cash given a desire to have it ready to easily deploy should equities fall further. We maintain our overweight to the New Zealand dollar, estimating it to be 3% undervalued based on our short-term model. The USD remains expensive on long-term valuation metrics with many of Trump’s policies carrying downside risk for the USD through potential capital outflow.

IMPORTANT NOTICE AND DISCLAIMER

This publication is provided for general information purposes only. The information provided is not intended to be financial advice. The information provided is given in good faith and has been prepared from sources believed to be accurate and complete as at the date of issue, but such information may be subject to change. Past performance is not indicative of future results and no representation is made regarding future performance of the Funds. No person guarantees the performance of any funds managed by Harbour Asset Management Limited.

Harbour Asset Management Limited (Harbour) is the issuer of the Harbour Investment Funds. A copy of the Product Disclosure Statement is available at https://www.harbourasset.co.nz/our-funds/investor-documents/. Harbour is also the issuer of Hunter Investment Funds (Hunter). A copy of the relevant Product Disclosure Statement is available at https://hunterinvestments.co.nz/resources/. Please find our quarterly Fund updates, which contain returns and total fees during the previous year on those Harbour and Hunter websites. Harbour also manages wholesale unit trusts. To invest as a wholesale investor, investors must fit the criteria as set out in the Financial Markets Conduct Act 2013.