Key market movements

Global equities rebounded strongly in April, with the MSCI All Country World Index (ACWI) advancing 6.7% in unhedged New Zealand dollar terms. Hedged investors experienced a more pronounced gain, with the ACWI rising 9.0% in hedged NZD terms, as the New Zealand dollar appreciated over the month.

Australasian equities missed the April rally, underperforming global peers. The S&P/NZX 50 Gross Index (including imputation credits) fell 0.1%, reflecting cautious company updates due to higher costs and a fall consumer confidence. Australian equities delivered better returns, with the S&P/ASX 200 Index up 2.2% in Australian dollar terms, or 3.7% for New Zealand dollar investors.

Fixed income returns were positive for the month, with the Bloomberg NZ Bond Composite Index returning 0.4% and the Bloomberg Global Aggregate Bond Index (hedged to NZD) advancing 0.2%, as robust earnings and risk-on sentiment drove credit spreads tighter.

Key developments

The balance of macro risks shifted during April from acute escalation toward a more constrained, energy driven stagflationary mix. The month opened with markets focused on the probability of a prolonged supply shock as shipping through key energy routes remained disrupted and risk premia lifted sharply. As the month progressed, limited ceasefire arrangements reduced tail risks around outright supply loss but did not reverse the underlying repricing of energy. Growth risks eased at the margin, while inflation risks became more persistent through second round channels. This mattered for policy because it narrowed the space for central banks to lean against slowing activity without jeopardising inflation credibility. Markets responded less to individual events and more to the implied duration of higher input costs and the extent to which those costs were being absorbed versus passed through.

The impact of the Iran war remains concentrated in energy supply, shipping capacity and the cost of moving goods. The Strait of Hormuz disruption kept oil prices elevated and volatile through April, with flow on effects into transport, freight and some essentials. In the euro area, the first clear inflation imprint was March headline CPI rising to 2.5% year on year from 1.9%, driven by energy prices that were up 8.3% on a three-month basis. In the US, labour market cooling remained evident, with job openings falling almost 5% in February and the hiring rate dropping to 3.1%, the lowest since 2010. The US economy remains in good shape with ISM surveys consistent with ongoing economic expansion and stronger than expected US retail sales for March, corroborating recent bank earnings that suggest US households are coping better than expected with higher energy prices. The Chinese economy remains resilient, supported by exports and targeted policy support. Higher energy prices have raised import costs, but the domestic transmission was muted by excess capacity and subdued household demand.

Recent global central bank communication has sought to maintain inflation targeting credibility. The Fed’s stance was framed as holding policy steady while it assesses whether higher energy prices feed into broader inflation pressure, and while it looks for confirmation that earlier goods price pressures roll off rather than compound. That posture is consistent with a desire to avoid easing prematurely into a near-term inflation lift, but it is also not a signal of impending tightening. In Europe, messaging leaned more explicitly on the risk that inflation expectations become unanchored if the energy disruption persists, while also recognising that the growth hit from higher imported energy costs is immediate in an energy importing region. Australia stands out because underlying inflation was already firm before the energy shock intensified. February data showed trimmed mean inflation holding at 3.3% year on year and market services inflation running at 3.3% year on year. Across jurisdictions, the common element is that to maintain policy credibility and prevent inflation expectations from drifting higher likely requires an acceptance of weaker growth outcomes.

The RBNZ signalled it had time to assess the impact of the Iran war. The OCR was held at 2.25%, with communication that it is prepared to look through the first-round impact of higher energy prices on near term inflation while standing ready to act if signs of persistence develop. The key test will be whether medium term inflation expectations and wage dynamics respond to higher headline inflation. The March quarter CPI outcome and the prospect of a larger fuel pass through in the June quarter increase the risk that expectations drift higher, particularly if freight and transport costs broaden into food and other non discretionary items. At the same time, the combination of weak confidence, a contracting services pulse and softening hiring intent supports the view that demand conditions can limit pass through and contain second round effects. If inflation expectations remain anchored and core inflation stays contained, holding policy through a near term headline inflation spike is consistent with the RBNZ’s recently articulated framework. If expectations rise materially or core inflation re accelerates, the tolerance to look through falls, and the policy response would need to be timely to protect credibility.

What to watch

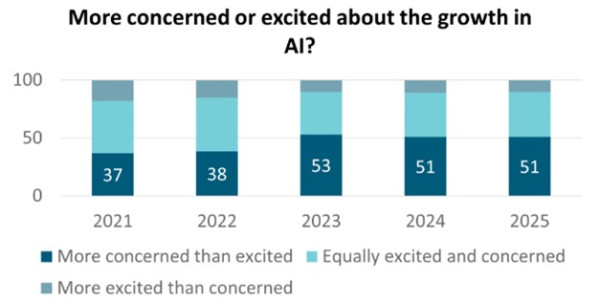

Source: Strategas, Pew Research Centre

A widening perception gap is emerging when it comes to AI. While markets continue to treat AI as a durable macro and earnings driver – supporting US equity leadership and sustained capital investment in data centres, energy and infrastructure – public opinion remains more cautious. Pew Research shows Americans are more concerned than excited about AI’s societal impact, reinforcing the case that the pace of AI adoption is likely to be shaped as much by regulation, energy constraints and social acceptance as by technological progress.

Market outlook and positioning

The global outlook remains dominated by developments in the Middle East, but markets have increasingly shifted from pricing worst‑case escalation scenarios to debating the duration and persistence. Ceasefire announcements have reduced immediate tail risks, yet physical disruption to energy and shipping routes remains meaningful. Oil prices have stayed elevated, and freight, insurance and logistics frictions continue to feed into costs. The key issue for markets is no longer whether there is an energy shock, but whether it fades quickly enough to avoid embedding broader inflation pressure.

That distinction matters for central banks. Policymakers have been clear that temporary energy price spikes can be looked through, but persistence would test inflation credibility. Recent commentary has reinforced a cautious, data dependent stance rather than a mechanical policy response. Markets, however, continue to price a relatively aggressive tightening path in several economies. This tension between softer growth signals and inflation risk is likely to keep rates markets volatile, particularly at the front end, as investors reassess how much tightening is ultimately required.

Global equity markets have rebounded strongly, supported by resilient US activity data, a strong start to company reporting season and renewed momentum in technology related sectors. The rally reflects confidence that earnings can absorb higher input costs in the near term and that growth, particularly in the US, remains sufficiently robust. However, conviction beneath the surface is uneven. Equity performance has been increasingly concentrated, suggesting investors are discriminating between companies with pricing power and structural growth and those more exposed to margin pressure.

Regional divergence is becoming more pronounced. The United States appears better insulated from the energy shock given its domestic energy production and stronger demand backdrop, while parts of Europe and Asia face a sharper growth inflation trade off. China has continued to show signs of stabilisation, supported by exports and improving industrial profitability, which may help offset some global headwinds. For Asia Pacific economies, higher energy costs and disrupted supply chains represent a more direct drag on activity, reinforcing relative dispersion across markets.

Overall, the macro environment points to ongoing volatility rather than a return to benign conditions. Growth is slowing but not collapsing, inflation risks remain two sided, and policy flexibility is constrained. In this setting, markets are likely to oscillate between optimism around earnings resilience and concern about policy and cost pressures.

Within equity growth funds Harbour’s strategy remains to be patient, position for a range of scenarios and to be selective, focusing on quality growth. We continue to focus on companies delivering earnings per share growth, particularly where that earnings growth has the potential to be higher and last for longer than consensus expectations allow for. We continue to see the secular (less dependent on economic activity) tailwinds of digitisation, disruption, de-carbonisation, and demographic changes as supporting company earnings. Our growth funds are overweight healthcare (predominantly via NZ retirement village investments where returns are expected to improve as supply and demand conditions stabilise and operational efficiency improves, and diagnosis businesses which have world class products and services), information technology (where there is potential to exceed user growth expectations), and select financials.

In fixed interest portfolios, our key strategy relates, as it has for much of the last 12-24 months, on the 1 to 5 year sector of the market, where monetary policy expectations are reflected. A phase of thin liquidity has enabled swap yields to rise, effectively pricing in a steady rise in the OCR to 3.5% by June 2027. We see this being at the higher end of likely outcomes and accordingly this becomes an attractive maturity rage to invest into, as realised OCR rates through time may not be this high.

Elsewhere in the portfolio we retain a holding in inflation-indexed bonds, which will enjoy a strong positive additional yield, which arises from the jump in inflation that we will see over the next 6 months. We have moved to an underweight position in longer maturity NZ Government Stock, as this sector may face pressure around the time of the budget, or if global concern about fiscal deficits increase from an already elevated level.

In aggregate, risk positions vis-a-vis the benchmark are not especially large. This reflects a deliberate decision to be more cautious in an environment of heightened volatility and uncertainty.

In the Income Fund, we have retained a modest underweight to Australasian equities, while reinstating a modest exposure to global equities. Fixed interest exposure is aligned with fixed interest portfolios.

In multi-asset funds, we are overweight global equities as an Iran resolution becomes more likely and underweight Australasian equities. Global equities should outperform Australasian equities given the US (which makes up almost 70% of the MSCI ACWI) is much better insulated from the energy shock. We are overweight domestic fixed income, with continued pricing of hikes inconsistent in our view with the spare capacity in the economy. We remain underweight global fixed income where there is greater fundamental support for higher yields. We maintain our overweight to the New Zealand dollar, estimating it to be undervalued based on our short-term model. The USD remains expensive on long-term valuation metrics with many of Trump’s policies carrying downside risk for the USD through potential capital outflow.

IMPORTANT NOTICE AND DISCLAIMER

This publication is provided for general information purposes only. The information provided is not intended to be financial advice. The information provided is given in good faith and has been prepared from sources believed to be accurate and complete as at the date of issue, but such information may be subject to change. Past performance is not indicative of future results and no representation is made regarding future performance of the Funds. No person guarantees the performance of any funds managed by Harbour Asset Management Limited.

Harbour Asset Management Limited (Harbour) is the issuer of the Harbour Investment Funds. A copy of the Product Disclosure Statement is available at https://www.harbourasset.co.nz/our-funds/investor-documents/ Harbour is also the issuer of Hunter Investment Funds (Hunter). A copy of the relevant Product Disclosure Statement is available at https://hunterinvestments.co.nz/resources/.

Please find our quarterly Fund updates, which contain returns and total fees during the previous year on those Harbour and Hunter websites. Harbour also manages wholesale unit trusts. To invest as a wholesale investor, investors must fit the criteria as set out in the Financial Markets Conduct Act 2013.