Key market movements

Global equities continued the rally in May adding another 3.4% in NZD-unhedged terms (and 5.1% in NZD-hedged terms as the New Zealand dollar strengthened through the month). Emerging markets outperformed through the month (+9.7%), with AI-exuberance fuelling extraordinary returns from Korea and Taiwan.

The New Zealand market staged a bit of a resurgence, with the S&P/NZX 50 Gross Index (including imputation credits) returning 2.7% over the month. Strong results from the larger end of the market supported returns. Australian equities were softer, with the S&P/ASX 200 Index up 1.1% in Australian dollar terms and -0.4% in New Zealand dollar terms.

Fixed income returns were positive again for the month, with the Bloomberg NZ Bond Composite Index returning 1.3% and the Bloomberg Global Aggregate Bond Index (hedged to NZD) advancing 0.5%, as the prospect of relief from the most acute phase of the energy crisis helped drive fixed income yields lower, following the sharp rise earlier in the month.

Key developments

The Iran conflict remained a defining macro backdrop across May. Nearly twelve weeks into the conflict, the Strait of Hormuz remained effectively closed to most shipping despite an ongoing ceasefire. Cumulative supply losses from Gulf producers exceeded one billion barrels, with over 14 million barrels per day shut in, the largest disruption in the history of the global oil market. Brent crude held near US$110 per barrel. Risk assets rallied mid-month after reports suggested the United States and Iran were close to agreeing a framework for broader peace negotiations, but that optimism faded quickly following renewed strikes, which underscored the fragility of the situation. The Trump-Xi summit in Beijing marked a clear attempt to stabilise a strained US-China relationship rather than reset it. Discussions covered an extension of the trade truce and cooperation to keep the Strait of Hormuz open. Outcomes were modest, with reduced near-term escalation more likely than a structural shift, but ongoing uncertainty around technology controls and Taiwan kept a geopolitical risk premium embedded in global assets.

Global macro signals remained challenging, led by renewed upside pressure in US inflation. April CPI surprised on the upside, with headline inflation rising to 3.8% year on year, its highest level in nearly three years, while core inflation lifted to 2.8%. The acceleration was driven primarily by energy, reflecting higher oil prices following renewed Middle East tensions, though services inflation also remained sticky. Bond markets responded quickly, with US Treasury yields pushing higher across the curve and expectations for Federal Reserve rate cuts in 2026 further pared back. Global bond yields pushed materially higher over the month as investors reassessed the mix of solid growth and high inflation. Markets became more open to higher term premia given ongoing fiscal deficits and rising bond supply, particularly in the United States where there were no clear signs of slower growth. In New Zealand, the RBNZ held the Official Cash Rate at 2.25% at its May Monetary Policy Statement, with Governor Breman's casting vote delivering the on-hold result. The projected OCR track showed a cumulative increase of 60 basis points by year-end, and markets moved to fully price three rate hikes by December.

A busy local earnings period supported strong NZ equity market performance, underpinned by positive results from several index heavyweights representing roughly a third of the NZX50 by market capitalisation. Results were generally solid to in-line and came without the negative surprises that had been feared, supporting strong share price performances in Ryman Healthcare and Mainfreight. Fisher and Paykel Healthcare was another standout, where stronger-than-expected margins and resilient growth drove a sharp share price reaction. Air New Zealand continued to signal very challenging trading conditions, with ongoing cost pressures and the likelihood of further capacity reductions across the network as the airline manages fuel costs and aircraft availability. Mercury hosted a Geothermal Investor Day outlining a NZ$75 million appraisal drilling programme at Rotokawa and Ngā Tamariki, with projects that could underpin up to NZ$1 billion of capital investment and deliver around 1 TWh of additional baseload electricity generation by 2030.

Equity market concentration remained front of mind as the AI cycle continued to evolve. Nvidia's latest result underscored the expanding value chain to infrastructure providers, with power, data centre and chip demand continuing to set the pace for returns. Memory-chip makers SK Hynix and Micron Technology joined an elite group of companies with market values exceeding US$1 trillion during the month. Micron's trailing 12-month return was over 950% at the end of May, whilst SK Hynix was up over 1000% in the same period. Hyperscalers now appear constrained by power availability, delivery certainty and operational capability rather than capital. The defensive layer of the AI value chain is increasingly less about models and silicon and more about electrons, grid access and trusted delivery at scale, supporting the view that the build-out remains a multi-year infrastructure task.

What to watch

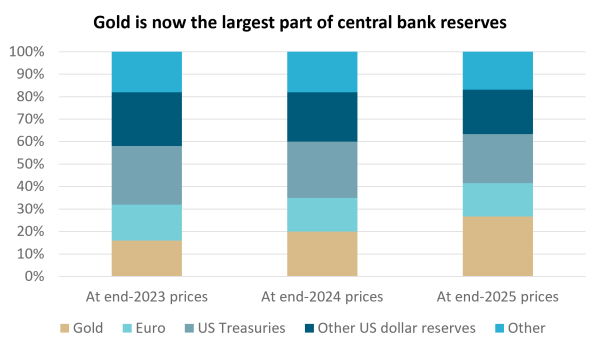

An interesting report was published by the European Central Bank, which showed that gold has replaced US government bonds to become the top global reserve asset by market value. Per the report, at the end of 2025, gold accounted for 27% of official foreign reserves compared to US treasuries at 22% and the Euro at 15%. This was driven by a strong rally in the gold price last year and sustained buying by central banks as they try to diversify away from the US dollar.

Source: European Central Bank

Market outlook and positioning

During May the balance of macro risks shifted away from near‑term growth disappointment and toward persistence risks around inflation, funding costs and policy credibility. Incoming data and policy communication reduced confidence that disinflation will proceed smoothly once energy and supply shocks fade. Markets increased the probability that restrictive monetary policy will need to be maintained for longer, even in places where activity momentum is already slowing.

At the global level, the dominant development was the renewed upward pressure on long‑end yields, driven by a combination of firmer realised inflation and large fiscal funding needs. Headline inflation prints were influenced by energy and trade‑related costs, but the underlying concern was pass through to broader prices. Central banks signalled tolerance for near‑term growth weakness if required to protect inflation targeting credibility. This stance limited the extent to which weaker activity data translated into easier financial conditions.

The divergence between economies is becoming clearer and provides useful context for portfolio positioning. US consumption remained resilient despite higher energy costs, consistent with an economy operating at or near capacity and supportive of a measured monetary policy approach. Economies with greater energy dependence, including the euro area and parts of Asia, face a more complex backdrop of cost pressures and slowing activity. Nonetheless, the broad-based repricing of yields reflects a global adjustment toward more sustainable long-term equilibria, and the differentiation across regions creates meaningful opportunity for active allocation.

Global equities continue to benefit from a strong and broadening earnings backdrop. Results through the first half of 2026 have materially outpaced expectations, with a higher than average proportion of reporting companies beating forecasts. Earnings upgrades have followed, reflecting resilient demand, improved margins, and the sustained tailwind from AI-related capital expenditure. Technology has led the way, though the breadth of profit growth is widening across sectors and regions. Forward earnings estimates have moved higher over the course of the year, providing a fundamental basis for continued market support.

The RBNZ held the Official Cash Rate at 2.25% at its May MPS - just. The MPC vote was split 3:3 with the 3 internal members voting to keep the OCR unchanged, while the 3 external members preferred a 25bp increase. Governor Anna Breman's casting vote ultimately delivered the on-hold result. While there was disagreement amongst the Committee on timing of hikes, there was broad agreement that hikes were imminent as the RBNZ looks to limit the prospect of second round inflation effects from higher energy prices, accepting a period of sub-trend economic growth. The RBNZ's projected OCR track now shows a cumulative increase of 60 basis points by year-end and a further approximately 40 basis points by end-2028. Markets have moved to fully price in three rate hikes by December, with an approximately 95% chance of a hike in July.

The NZ government resisted the temptation of giving out pre-election lollies in Budget 2026. It opted instead for fiscal restraint that should see a surplus achieved in fiscal year 2029, a year earlier than previously projected. Admittedly, these forecasts were helped by optimistic growth projections that deliver higher tax revenues over the next four years. The implication for the government bond programme was a $6bn reduction relative to the previous forecasts but the overall amount of issuance is still large at $124bn over the next four years.

Within equity growth funds our strategy remains to be patient, position for a range of scenarios and to be selective, focusing on quality growth. We continue to focus on companies delivering earnings per share growth, particularly where that earnings growth has the potential to be higher and last for longer than consensus expectations allow for. We continue to see the secular tailwinds of digitisation, disruption, de-carbonisation and demographic changes as supporting company earnings. Our growth funds are overweight healthcare, predominantly via NZ retirement village investments where returns are expected to improve as supply and demand conditions stabilise and operational efficiency improves, also Australian pharmaceutical and diagnostics businesses with world-class products and services supporting long-term growth. The funds are also overweight select financials (where Challenger may benefit from improved capital efficiency, Infratil from data centre growth, and Macquarie from stronger transaction activity), and materials (where BHP and Rio Tinto may continue to see positive earnings from strong commodity pricing). We are underweight utilities, communication services and real estate, where valuation multiples remain full relative to modest earnings growth prospects.

In fixed interest, the market continues to price in a more aggressive OCR rate track than the RBNZ, seeing a terminal of close to 50bps above, near 3.75%. While near term hikes are likely necessary given the current low level of policy settings, we continue to view market pricing as overestimating the extent of tightening required. Portfolios continue to hold a moderately long duration position, centred in the 1-5-year tenors.

Positioning in credit continues to focus on higher quality, shorter dated bonds. Corporate credit spreads are historically expensive, particularly in issues longer than 3 years. Issuance in credit markets has increased recently, with highly rated AAA overseas issuers finding solid demand, despite the relatively tight spreads achieved over NZ government debt. While upcoming issuance in retail format will deliver an attractive absolute yield and support demand, we remain somewhat guarded as the premiums look insufficient and there are better options in other, higher quality names.

In aggregate, risk positions vis-a-vis the benchmark are not especially large. This reflects a deliberate decision of prudent risk management in an environment of heightened uncertainty.

In the Income Fund, allocation to equities is very close to a neutral 32% weight. In fixed interest, the strategy is in line with the bond strategy described above. We continue to hold inflation-indexed bonds, which provide an attractive risk mitigation feature if inflation keeps rising and puts pressure on other fixed interest securities and equities simultaneously.

In multi-asset funds, we are overweight global equities and underweight Australasian equities on relative earnings prospects. Global equities should outperform Australasian equities given the US (which makes up almost 70% of the MSCI ACWI) is much better insulated from the energy shock. We are overweight in domestic fixed income, with market pricing of the OCR to reach 3.75% inconsistent with our view of the spare capacity in the economy. We remain underweight global fixed income where there is greater fundamental support for higher yields. We maintain our overweight to the New Zealand dollar, estimating it to be undervalued based on our short-term model. The USD remains expensive on long-term valuation metrics with many of Trump’s policies carrying downside risk for the USD through potential capital outflow.

IMPORTANT NOTICE AND DISCLAIMER

This publication is provided for general information purposes only. The information provided is not intended to be financial advice. The information provided is given in good faith and has been prepared from sources believed to be accurate and complete as at the date of issue, but such information may be subject to change. Past performance is not indicative of future results and no representation is made regarding future performance of the Funds. No person guarantees the performance of any funds managed by Harbour Asset Management Limited.

Harbour Asset Management Limited (Harbour) is the issuer of the Harbour Investment Funds. A copy of the Product Disclosure Statement is available at https://www.harbourasset.co.nz/our-funds/investor-documents/ Harbour is also the issuer of Hunter Investment Funds (Hunter). A copy of the relevant Product Disclosure Statement is available at https://hunterinvestments.co.nz/resources/.

Please find our quarterly Fund updates, which contain returns and total fees during the previous year on those Harbour and Hunter websites. Harbour also manages wholesale unit trusts. To invest as a wholesale investor, investors must fit the criteria as set out in the Financial Markets Conduct Act 2013.