- SpaceX is targeting a $1.8 trillion valuation in what would be the largest IPO in history, and the sheer scale of the listing may reshape how major stock indices work.

- Index providers including Nasdaq, FTSE Russell, and potentially S&P have rewritten their inclusion rules specifically to accommodate SpaceX, forcing many passive funds to buy the stock almost immediately after listing.

- With only around 5% of shares available to the public, a wave of forced buying from trillions of dollars of index-tracking capital will chase a scarce float, with consequences for price discovery and portfolio concentration.

SpaceX is expected to begin trading on Nasdaq on 12 June, targeting a valuation of around $1.8 trillion – the largest IPO ever undertaken. This is more than a big tech listing. It raises some genuinely interesting questions about how passive investing works, who gets to set the rules, and what it means for the trillions of dollars of retirement savings tracking major indices. For many investors, index funds are the backbone of their portfolios. The SpaceX listing affects all of them.

Before getting to the market mechanics, three things about SpaceX are worth flagging upfront. First, governance: Musk retains complete operational control, with shareholder voting rights and fiduciary duties effectively eliminated. Large pension funds have described it as "the most management-favourable governance structure ever brought to the US public markets at this scale" – we would be hard pressed to argue otherwise. Second, valuation: SpaceX lost $4.9 billion on $18.7 billion in revenue last year yet is seeking to list at a valuation which is around 100 times revenue. For context, Nvidia at the peak of its AI rally traded at 40 to 45 times revenue. Third – and most relevant for what follows – free float: only around 5% of shares will be available to public investors at IPO, with the remainder subject to lockup restrictions.

The float issue cannot be separated from a story that has largely flown under the radar: how quickly the major index providers have rewritten their rules ahead of this listing. On 30 March, Nasdaq cut the waiting period for index inclusion from three months to just 15 trading days for any newly listed company in the top 40 by market cap, and dropped the previous 10% minimum float requirement entirely, this announcement conveniently came right when Nasdaq was confirmed as the listing location for the IPO. FTSE Russell followed on 26 May, confirming that qualifying IPOs can enter the index after just five trading days. S&P Dow Jones's consultation on waiving its 12-month seasoning requirement, profitability test, and minimum float threshold closed on 28 May – if adopted, these changes take effect 8 June, four days before SpaceX is due to list. There is a defensible case for much of this: at $1.8 trillion, SpaceX would be one of the largest companies in the world from day one, and if an index is meant to represent the investable market, it should probably include its largest members promptly. But we think it is worth asking whether index providers are adapting sensibly to a structural shift in how large companies come to market, or simply rewriting the rulebook because one influential CEO and company asked them to.

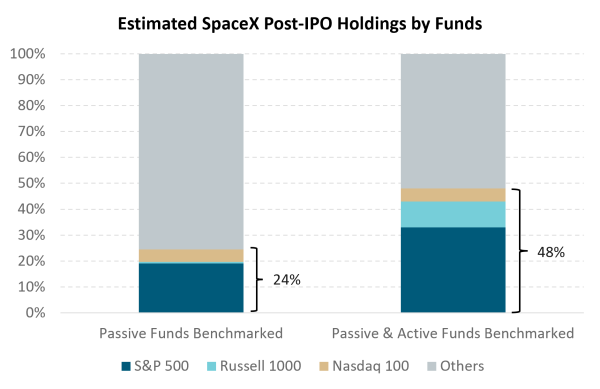

That question matters because index inclusion is not a neutral act – it is a mandate to buy. Bloomberg Intelligence estimates that passive S&P 500 funds alone could be required to absorb around 19% of all publicly available SpaceX shares within six months of listing, with the stock entering at approximately the sixth-largest index position. Add Nasdaq-100 and Russell 1000 index trackers and passive benchmarked funds reach around 24% of the entire public float. Factor in active managers benchmarked to these same indices – who face real career risk from being materially underweight a top-10 stock – and the total reaches approximately 48% of SpaceX's entire initial public float.

Source: Bloomberg

The consequence of that forced buying is amplified by the thin float. Todd Sohn, chief ETF strategist at Strategas, put it well: it will feel "almost a little frantic, because you're dealing with ETFs and passive products that are tracking trillions of dollars of assets and yet you only have 5 per cent of float available." His point on the endgame is equally direct: "If SpaceX is up 100 per cent the week after the IPO, and they have to buy it, they have to buy it. They can't discriminate." This is less a criticism of the fund managers involved than an observation about the mechanics – the managers are doing exactly what their mandates require. A market where forced, price-insensitive buying chases a scarce float is not conducting price discovery. Research published earlier this year found that short index seasoning periods cause prices to spike at inclusion and then fall by as much as 10% in the months that follow.

The Aramco IPO of 2019 offers some useful context. Saudi Aramco listed at a market cap of $1.877 trillion – larger than Apple at the time – but with a float of just 1.5%. The energy sector's weight in Saudi indices jumped from under 1% to 6.5% overnight, and passive investors acquired a large position in a state-controlled oil company whether they chose to or not. The SpaceX situation shares the structural logic, but the systemic stakes are considerably higher. Aramco sat within emerging market benchmarks. SpaceX would sit at the core of the S&P 500, Nasdaq-100, and Russell 1000 – the benchmarks that underpin the vast majority of retirement savings globally, including through KiwiSaver and Australian superannuation funds.

On the lockup side, SpaceX has structured its restrictions differently from the standard 180-day cliff. Rather than a single expiry date, the S-1 filing reveals a tiered, rolling release schedule where insider shares unlock in tranches from the first quarterly earnings release through to the 180-day mark. The upside is a reduced risk of the sharp price declines that have historically followed concentrated lockup expirations. The flip side is that each tranche release grows the free float, which triggers float-adjustment mechanisms in major indices – meaning SpaceX's index weight rises with each release and passive funds must buy more shares to stay on benchmark. The rolling lockup spreads the supply pressure out, but does not eliminate it.

This dynamic does not end with SpaceX. Anthropic (the maker of Claude AI) filed a confidential S-1 with the SEC on 1 June, targeting a listing near a $965 billion valuation in October 2026. OpenAI, valued at approximately $852 billion at its last funding round, is preparing its own offering before year-end. At combined current valuations, the three companies would bring close to $3.6 trillion in new market capitalisation to public investors within months of each other. The index rules are already changed. When Anthropic and OpenAI list, passive funds will face the same forced buying mechanics – into whatever float is available, at whatever price the market sets.

We do not think this is necessarily an argument that SpaceX will be a poor investment – the Tesla precedent would suggest otherwise. S&P's decision to exclude Tesla from its index for a decade cost passive investors meaningful returns as the stock appreciated 230-fold. There is a genuine argument that rules designed for a different era of capital markets were due for revision.

The more interesting question, in our view, is structural. What we are watching is a rewriting of the rules that underpin passive investing – the premise that index funds provide neutral, low-cost exposure to the market as it exists. When the largest private companies in the world can negotiate their index inclusion terms as a condition of listing, and the result is that hundreds of billions of dollars of retirement savings are directed into a specific stock at a specific moment regardless of price, the neutrality of the index is no longer quite as given as it once seemed. For investors who have chosen active management precisely because it allows a portfolio manager to exercise judgment – to own SpaceX at a price they consider appropriate, or not at all – that distinction has rarely felt more relevant.

IMPORTANT NOTICE AND DISCLAIMER

This publication is provided for general information purposes only. The information provided is not intended to be financial advice. The information provided is given in good faith and has been prepared from sources believed to be accurate and complete as at the date of issue, but such information may be subject to change. Past performance is not indicative of future results and no representation is made regarding future performance of the Funds. No person guarantees the performance of any funds managed by Harbour Asset Management Limited.

Harbour Asset Management Limited (Harbour) is the issuer of the Harbour Investment Funds. A copy of the Product Disclosure Statement is available at https://www.harbourasset.co.nz/our-funds/investor-documents/. Harbour is also the issuer of Hunter Investment Funds (Hunter). A copy of the relevant Product Disclosure Statement is available at https://hunterinvestments.co.nz/resources/. Please find our quarterly Fund updates, which contain returns and total fees during the previous year on those Harbour and Hunter websites. Harbour also manages wholesale unit trusts. To invest as a wholesale investor, investors must fit the criteria as set out in the Financial Markets Conduct Act 2013.