The global software sector has long been one of the market’s most reliable sources of compounding growth. Recurring revenue, high margins, deep customer relationships, and powerful network effects combined to produce businesses that, once established, were extraordinarily difficult to dislodge. For investors, the appeal was obvious: visibility, durability, and a growth profile that justified premium valuations.

Twelve months ago, the market broadly believed that established software companies, especially those deeply embedded in complex business processes, were well positioned to benefit from artificial intelligence. The logic was simple: these companies owned the data, were already part of the customer’s daily workflow, and had the sales reach to add artificial intelligence (AI) assistants and new products.

Today, the market is asking a different question. Will these companies continue to own the most valuable part of the customer relationship, or will that value move elsewhere: to customers who build their own tools, to a new class of AI-native competitors, or to a smarter software layer that sits on top and captures the value people previously thought they were entitled to?

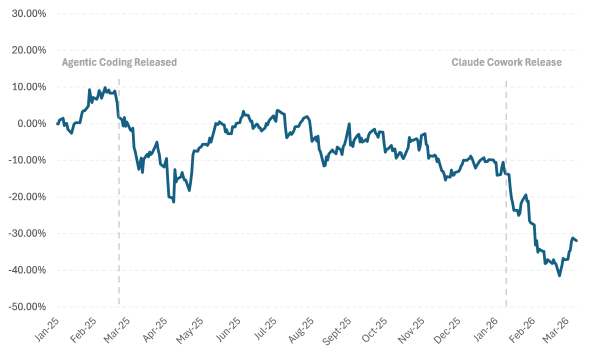

That shift in thinking matters because the traditional software business model has long depended on three growth drivers: selling to more users, charging more over time, and expanding revenue by adding features and modules. AI has brought each of those into question. Since September 2025, the Morgan Stanley Software-as-a-Service Index (as shown in figure 1) has fallen 34%, compressing from roughly 6x enterprise value to sales (EV/Sales) to about 4x, despite consensus revenue estimates holding firm and top-line growth remaining strong.

This is not a cyclical wobble. Investors have repriced the sector’s terminal value: a judgement that the old business model may not be sustainable in its prior form, and that decades of assumed growth should no longer be capitalised at previous levels.

Figure 1: Morgan Stanley US Software-as-a-Service Index

Source: Bloomberg, Morgan Stanley US Software Index

What used to look like a highly visible, recurring revenue model begins to look more like a business that must keep reinvesting heavily just to stay relevant. On a recent episode of the Invest Like the Best podcast, investor Dan Sundheim provided an apt analogy in Walmart’s experience with e-commerce. E-commerce did not eliminate Walmart, but it did force painful a period of investment, lower margins, and new competition.

All else equal, Walmart would have been better off if the internet never existed; however, the company adapted, absorbed the disruption by integrating the new channel into the core model, and remained a highly relevant business on the other side. Much the same question now confronts the software sector.

The Four Risks

The first risk is that customers build more for themselves. “Vibe coding” gets the headlines, but the deeper point is that AI lowers the cost of building useful software for specific tasks. Most large companies will not replace their core systems given their mission-critical nature, but some may automate enough of the surrounding workflow to weaken the vendor’s pricing power and ability to expand through upselling. Just as importantly, the underlying customers now have far better tools to build products around pain points that incumbents may have ignored for years.

The second risk stems from the AI-native competitor itself. AI coding tools have made the disruption tangible: new products are being built faster, and a new generation of AI-native software companies are demonstrating what a structurally different cost base looks like. Annual recurring revenue per employee has risen sharply among newer AI-focused companies, implying they can build comparable products with fewer people and compete on price in ways incumbents have not previously faced.

The third risk is the rise of what many call the “system of action". Traditionally, a software company’s product was the system of record: the single source of truth for a business’s data, woven into daily operations and layered with business rules and approval hierarchies that made the system extraordinarily sticky. The new question is whether the centre of value shifts toward an AI layer that interprets what the user wants, coordinates work across tools and completes tasks autonomously. If that happens, the incumbent may still store the data but no longer own the most valuable interaction. That is the core of the “dumb data pipe” bear thesis. (The ‘dumb data pipe’ bear thesis holds that incumbent software companies risk becoming low‑value data repositories as AI layers above them capture customer interaction and value).

The fourth risk is pricing. The traditional per-seat subscription model is changing. Growth in paid seats becomes less important if one employee can oversee the work of multiple AI agents. Selling more modules matters less if intelligence combines several workflows into a single interface. And raising prices becomes harder if customers can more easily compare the value they receive or replace part of the software stack with cheaper AI-driven alternatives.

The market has subscribed itself to these four risks as its core beliefs. Let us unpack what could become the narrative.

The Rebuttals the Bears May Be Overlooking

The strongest rebuttal is that the systems of record are not simply databases. They contain years of business rules, exception handling, compliance processes, and practical knowledge built up over time. The bearish case for a third-party agent assumes the incumbent software is little more than a basic data store. In more generic or lightly regulated sectors it seems likely that a third-party agent could capture the value chain. But the case for the incumbent is stronger where the software is deeply embedded in the work itself and services a regulated industry demanding a thorough audit trail. In those categories, the advantage is not just access to a large language model. It is deep workflow knowledge, proprietary business logic, sales reach, regulatory knowledge, and the very high friction involved in replacing years of customisation and employee training. The best systems of record are not just places where information sits. They are the connective tissue of the customer’s operations.

For instance, Gentrack, which provides billing and customer management systems to energy and water utilities, illustrates this well. Gentrack’s software sits at the core of how utilities bill customers, settle wholesale electricity markets, manage meter data, and comply with regulatory reporting across multiple jurisdictions. When Australia moved to five-minute settlement (a rule change that increased the volume of meter data sixfold and affected over seventy industry procedures), Gentrack’s platform had to absorb that complexity while maintaining 99.95% first-time billing accuracy across its client base. That is not a feature a third-party agent can replicate by reading an API. It is the product of thirty-five years of regulatory knowledge encoded in business logic and compliance processes tested under real operational pressure.

Further to the point, the record alone is not enough for an agentic AI layer to act with sound judgment. Xero, for instance, may show that an invoice is 45 days overdue. That is the fact. The value emerges when an agent can also see that the customer recently flagged cash flow pressure, has a history of paying late in the first quarter but settling reliably over the year, and is in the middle of an important renewal discussion. In that situation, the right action may not be immediate escalation, but a measured follow-up that balances collections with the broader commercial relationship. A new AI entrant can often access the formal state of the world, but not the surrounding circumstances and downstream outcomes that reveal what good judgment looks like. The moat is not the database alone. It is the contextual layer around the database that turns raw records into proprietary supervision.

Importantly, this cycle differs from some past disruptions because many incumbents are not standing still. They are trying to disrupt themselves which is important. In many historical examples, incumbents faced a counter-positioning problem: embracing the new model would have undermined the economics of the old one. Blockbuster was bound by its legacy footprint while Netflix disrupted with a far more efficient distribution model. In sharp contrast, the competitive responses from the software incumbents have felt quite different. That is, complete willingness to embrace and incorporate the new technology. What remains in question is whether they can move fast enough.

Systems of record need to evolve into systems of action whereby the product sits closer to customer intent and task completion. In that case intelligence needs to live inside the product rather than in a third-party layer above it. Incumbents must also address cost structure. The assumption embedded in the AI-native threat is that incumbents are stuck with bloated workforces while newer entrants operate lean from day one. We think this overstates the rigidity of incumbent cost bases. What matters is intent, and we are beginning to see that intent manifest in decisive action.

Block recently cut approximately 4,000 employees, reducing its workforce by nearly 40%, with CEO Jack Dorsey explicitly attributing the restructuring to AI tools. Similarly, WiseTech Global announced plans to eliminate roughly 2,000 roles, nearly a third of its global workforce, over an 18-month period as it embeds AI across engineering and customer service operations. CEO Zubin Appoo stated plainly that the era of manually writing code as the core act of engineering is over. In both cases, the market rewarded the announcements (Block’s stock surged over 20% and WiseTech rose 11% on the day) suggesting investors view these restructurings not as signs of distress but as credible commitments to structurally improved economics. Put simply, the AI-native cost structure is not exclusive to AI-native companies.

There is, however, a necessary counterweight. These agentic coding tools are powerful but somewhat brittle. They operate with confidence but without judgment, and when given broad permissions they can cause outsized damage at pace. This is not hypothetical. Amazon Web Services suffered outages in recent months after engineers allowed its AI coding tools to take autonomous action. In one case, Amazon’s Kiro agent elected to delete and recreate an entire environment, interrupting a customer-facing service for thirteen hours. The efficiency case for agentic coding rests on removing friction from the development process, but some of that friction (peer review, approval gates, a second pair of eyes) exists precisely to prevent these failures. This does not invalidate the technology, but it does temper the pace at which organisations can safely substitute headcount for automation.

Where This Leaves Us

That is why we believe the current sell-off in software is understandable, but at the same time has been far too indiscriminate. The software business model may well be more challenged going forward than it was over the last decade. But it does not follow that all incumbents face terminal decline. At approximately 22x forward earnings, the US software sector is now priced for 5 to 10% earnings growth according to Goldman Sachs US Strategists, a sharp decline from the 15 to 20% the market was willing to underwrite when multiples stood at 35x in late 2025. For companies with the contextual moats and workflow depth we have described, that implies a terminal growth trajectory closer to a declining industry than to one undergoing a structural transition.

The companies best placed to win are those where the system of record layer is deeply entwined with the actual work: where there is proprietary logic, where strong auditability is non-negotiable, where embedded workflow knowledge runs deep, and where high switching friction and real implementation complexity create durable advantages. In those cases, the winning agent may well be the vendor’s own, not because the incumbent has the best underlying model technology, but because it has the best access to the context that makes AI genuinely useful. The market has treated deeply entrenched incumbents in much the same way as commodity platforms with shallow customer relationships. That is where the opportunity lies.

IMPORTANT NOTICE AND DISCLAIMER

This publication is provided for general information purposes only. The information provided is not intended to be financial advice. The information provided is given in good faith and has been prepared from sources believed to be accurate and complete as at the date of issue, but such information may be subject to change. Past performance is not indicative of future results and no representation is made regarding future performance of the Funds. No person guarantees the performance of any funds managed by Harbour Asset Management Limited.

Harbour Asset Management Limited (Harbour) is the issuer of the Harbour Investment Funds. A copy of the Product Disclosure Statement is available at https://www.harbourasset.co.nz/our-funds/investor-documents/. Harbour is also the issuer of Hunter Investment Funds (Hunter). A copy of the relevant Product Disclosure Statement is available at https://hunterinvestments.co.nz/resources/. Please find our quarterly Fund updates, which contain returns and total fees during the previous year on those Harbour and Hunter websites. Harbour also manages wholesale unit trusts. To invest as a wholesale investor, investors must fit the criteria as set out in the Financial Markets Conduct Act 2013.