- Global private credit headlines do not always reflect the structure and risk profile of the New Zealand market.

- Some of the features attracting scrutiny overseas, including intense competition, fund-level leverage and concentrated sector exposures, are less prevalent locally.

- Long-term outcomes will depend less on the asset class itself and more on manager discipline, portfolio construction and investor alignment.

The growth of private credit in New Zealand is a positive development, providing borrowers with more choice and investors with access to a maturing alternative asset class. At the same time, recent developments in global private credit markets – including fund closures, redemption pressures and increasing scrutiny of sector exposures – have been hard to ignore. It is natural that this prompts concern. Private credit has grown rapidly, and periods of stress often reveal where underwriting standards, leverage, or market structure have become stretched. These developments are worth taking seriously. However, it is equally important to distinguish between the global market, particularly in the US and Europe, and the structure of private credit in New Zealand. While there are areas of overlap, there are also some important differences that shape the risk profile.

A Less Competitive Lending Market

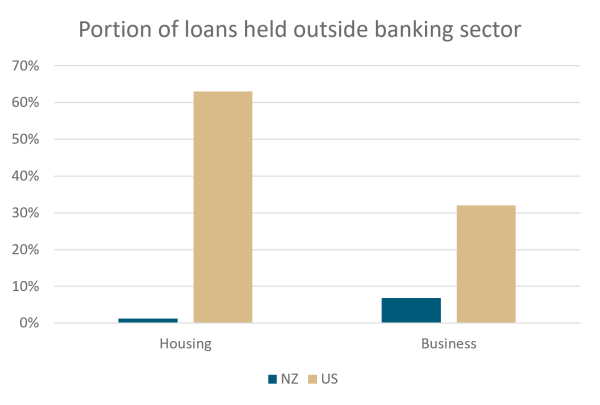

Corporate lending remains highly concentrated in New Zealand, dominated by four large Australian-owned banks. These institutions account for over 80% of lending and tend to operate with similar frameworks and risk appetites.

By contrast, in the United States, the lending market is significantly more fragmented. Thousands of banks participate in commercial lending, and there has been a sustained retreat of banks from segments such as leveraged lending. This has enabled private credit to grow rapidly, with hundreds of funds now competing to deploy capital.

The result is a very different competitive dynamic:

- In the US, borrowers can often access multiple competing lenders, including large-scale private credit funds managing tens or hundreds of billions of dollars.

- In New Zealand, both bank and non-bank options are far more limited, and private credit remains a relatively small part of the overall system.

This matters because competition influences underwriting discipline. In more competitive markets this often manifests in looser covenants, higher leverage, and tighter pricing. Over time, these dynamics have tended to be associated with weaker credit outcomes, including in the lead-up to the Global Financial Crisis (GFC). For example, in the US mid-market, uni-tranche lending spreads have compressed materially, typically moving from around 600–700bps post-GFC to nearer 450–550bps in more competitive periods.

New Zealand has not experienced this to the same degree. While competition does exist, it is meaningfully less intense, which tends to support more conservative structures. Historically, this has also contributed to lower loss experience through credit cycles, including periods such as the GFC, although outcomes are never guaranteed. Consistent with this, even globally realised default rates in private credit have typically remained in the low single digits, albeit with meaningful variation across sectors and underwriting quality.

Source: Consumer Financial Protection Bureau (2025); Reserve Bank of New Zealand (C5, S31), 2026; McKinsey & Company (2024), The Next Era of Private Credit

No Fund-Level Leverage

A second key difference is the use of leverage at the fund level. Many global private credit funds employ borrowing to enhance returns. This can take the form of subscription lines or asset-level leverage, which may not always be apparent from underlying borrower metrics. Not only does this also magnify losses, but it introduces an additional layer of risk as funds must refinance their own debt and there is potential for forced selling in stressed markets. New Zealand private credit funds, by contrast, are generally unlevered. It does not remove credit risk at the borrower level, but it avoids amplifying that risk through the fund structure.

Sector Exposure: Software and Data Infrastructure

A focal point of global concern has been exposure to software companies. Software has been one of the strongest growing sectors of the economy and its growth has occurred concurrently with the growth of private credit, so it is logical that software occupies a material share of private credit portfolios.

Precise data are difficult to obtain, in part because sector classification is inconsistent. Reported software exposure is often around 15–20% of private credit portfolios. However, more detailed analysis suggests the true exposure may be higher – closer to 20–30% – once companies classified as ‘business services’, ‘IT services’, or even parts of healthcare are included, reflecting the underlying role software plays across those sectors. Publicly-disclosed portfolios of business development companies are broadly consistent with this range, depending on classification approach. This matters because it means sector exposures may appear diversified, while still being driven by similar underlying business models.

Our exposure to software and data infrastructure in the Hunter private credit funds currently remains in the single digits and is broadly consistent with what we observe across New Zealand-focused portfolios.

Simplicity and Structure

The New Zealand private credit market is generally less complex than larger offshore markets. Transactions tend to involve simpler capital structures, fewer layers of debt, and clearer borrower profiles.

This can make risks easier to identify and manage. However, it is important not to overstate this point. While this can make risks easier to identify, simplicity does not eliminate risk. Outcomes remain driven by borrower quality, leverage, and structure.

A Shared Feature: Illiquidity and Confidence

Despite these differences, there is an important commonality between global and New Zealand private credit: the asset class relies on ongoing liquidity support. Private credit investments are inherently illiquid. Capital is typically committed for a defined period, and interim exit options are limited. This makes the stability of the investor base important.

A further feature of the New Zealand market has been the role of the Active Investor Plus (AIP) framework, which has contributed to the growth of private credit capital. This introduces an additional dynamic for fund managers. On one hand, it can lead to a degree of investor base concentration. On the other, AIP capital is typically associated with defined investment horizons, which can support more predictable capital flows compared to fully open-ended structures. As with all aspects of private credit, outcomes ultimately depend on how well these dynamics are understood and managed.

In this context, understanding both the structure of the assets and the structure of the investor base becomes critical in assessing risk.

Credit Risk in an Evolving Market

Recent developments in global private credit markets provide a useful reminder that credit risk cannot be eliminated and that periods of stress often reveal weaknesses in underwriting, portfolio construction or market structure.

While New Zealand shares some characteristics with larger offshore private credit markets, it also exhibits several important differences, including lower levels of competition, limited use of fund-level leverage, generally simpler transaction structures and lower exposure to some of the sectors currently attracting attention internationally.

These factors do not make the market immune to credit losses or economic cycles. Rather, they suggest that risk should be assessed through the specific characteristics of individual portfolios, managers and borrowers, rather than broad assumptions about the asset class as a whole.

As private credit continues to evolve in New Zealand, disciplined underwriting, transparent portfolio construction, and alignment between investor liquidity expectations and underlying assets will remain critical determinants of long-term performance.

IMPORTANT NOTICE AND DISCLAIMER

This publication is provided for general information purposes only. The information provided is not intended to be financial advice. The information provided is given in good faith and has been prepared from sources believed to be accurate and complete as at the date of issue, but such information may be subject to change. Past performance is not indicative of future results and no representation is made regarding future performance of the Funds. No person guarantees the performance of any funds managed by Harbour Asset Management Limited.

Harbour Asset Management Limited (Harbour) is the issuer of the Harbour Investment Funds. A copy of the Product Disclosure Statement is available at https://www.harbourasset.co.nz/our-funds/investor-documents/. Harbour is also the issuer of Hunter Investment Funds (Hunter). A copy of the relevant Product Disclosure Statement is available at https://hunterinvestments.co.nz/resources/. Please find our quarterly Fund updates, which contain returns and total fees during the previous year on those Harbour and Hunter websites. Harbour also manages wholesale unit trusts. To invest as a wholesale investor, investors must fit the criteria as set out in the Financial Markets Conduct Act 2013.