Article originally published 07 July 2026 by the NBR

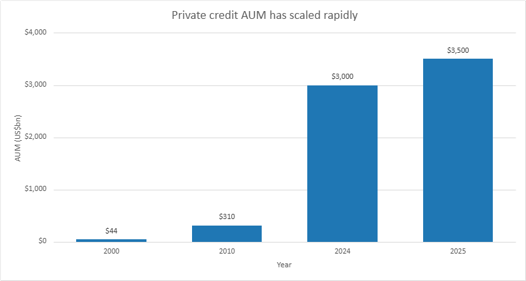

Over the past decade, private credit has evolved from a niche investment strategy into a mainstream source of funding for businesses globally. The global private credit market has reached $3.5 trillion in assets under management (AUM)*.

Source: AIMA reports & UBS/Pregin and AUM shown in US$bn

It’s worth acknowledging there has been some negative sentiment, but global growth of private credit is ultimately a business story. From the United States to Europe and Australia, private credit has become an increasingly important source of funding for businesses seeking capital to grow, acquire competitors, invest in infrastructure, or navigate periods of transition.

As the asset class has scaled, it has given companies access to capital that is often more flexible, more certain and better matched to their investment needs than traditional funding channels alone. Private credit has helped bridge that gap by providing bespoke debt capital, greater execution certainty and capital structures designed around the cash flow profile of the business or asset being funded. The benefit is not simply that more money is flowing into private markets; it is that more businesses can access the capital needed to build, expand and compete in sectors that are central to future productivity and growth.

The New Zealand Private credit market is maturing

While still relatively small compared to overseas markets, New Zealand's private credit market has developed significantly over the past couple of years. A growing number of private credit managers, institutional investors, family offices, iwi investment entities, wholesale investors, and KiwiSaver providers are allocating capital to private lending strategies.

This shift is also being supported by the maturing of the local market and by policy settings such as the Active Investor Plus visa programme, which has helped direct offshore investor capital toward productive New Zealand investments, including private credit.

The scale is becoming meaningful. After its first year, the Active Investor Plus programme had attracted almost $3.9 billion of total committed investment into New Zealand, including $1.49 billion already invested and a further $2.4 billion in the pipeline. Within that, private credit has been one of the larger allocation categories, approaching $900 million, with more than $480 million already deployed and a further $376 million committed to businesses looking to innovate and grow.

Historically, much of New Zealand’s private credit activity has been deployed into property-related lending, including development finance, construction lending, and other real estate secured exposures. That has been an important part of the market, but it does not represent the full potential of the asset class.

There are more than 20,000 businesses with 20 or more employees**, representing a meaningful pool of mid-market and larger borrowers that may benefit from more flexible capital than traditional bank lending alone can provide.

Many of these businesses are profitable, cash-generative, and well managed. Yet they may not fit neatly within conventional lending frameworks due to transaction complexity, timing requirements, industry characteristics, or capital structure considerations. As a result, businesses can find themselves with strong opportunities but limited access to appropriately structured capital. This is where private credit can play a meaningful role.

Private Credit can support New Zealand's growth sectors

While property lending has historically been an important part of New Zealand's private credit market, the opportunity extends well beyond real estate.

Private credit can and has started to support a wide range of sectors including technology, infrastructure, manufacturing, healthcare, business services and other operating businesses that require flexible sources of capital. Funding solutions include growth capital, acquisition finance, asset finance and working capital facilities tailored to a company's specific needs.

This can be particularly relevant for New Zealand's high-growth businesses. Reports such as Deloitte's Fast 50 and TIN (“Technology Innovation Network”) reports consistently showcase NZ innovative companies achieving strong growth across a broad range of industries. Many of these businesses require additional capital to scale, invest and expand but may not fit neatly within traditional lending frameworks due to their growth profile, transaction complexity or timing requirements.

For these companies, private credit provides an additional source of funding alongside traditional bank finance and equity capital. Well-structured debt solutions can help businesses pursue opportunities, invest in productive assets and fund growth while preserving ownership and flexibility.

As New Zealand continues to produce innovative, export-focused and high-growth businesses, demand for diverse sources of capital is likely to increase. A broader private credit market can help ensure these businesses have access to the funding needed to invest, create jobs and contribute to long-term economic growth.

Why New Zealand needs more sources of capital

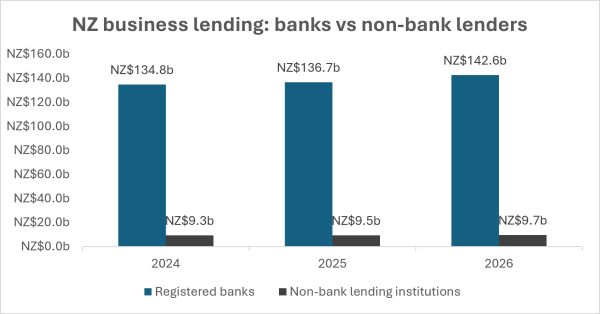

New Zealand has long benefited from a stable and well-capitalised banking system. The major banks continue to play a critical role in supporting businesses and the wider economy.

However, New Zealand remains one of the more bank-dependent economies in the developed world. For many mid-market businesses, particularly those undertaking acquisitions, succession transactions, or growth initiatives, there is often a funding gap between what traditional banks are willing to provide and what business owners are seeking.

Source: AIMA reports & UBS/Pregin and AUM shown in US$bn

Private Credit and Banks are partners, not competitors

Perhaps the most important point is that private credit should not be viewed as competing with banks. In reality, the most effective financing solutions often involve both. Banks continue to provide significant value through transactional banking, treasury services, foreign exchange solutions, interest rate hedging, trade finance, payments infrastructure, day-to-day banking relationships and senior secured lending.

Private credit providers can offer greater flexibility by having the ability to participate in either or both senior and subordinated lending, acquisition finance, growth capital, asset finance, transitional financing, special situations funding.

These capabilities are complementary rather than competing. In many international markets, private credit funds and banks regularly collaborate to deliver comprehensive financing solutions for borrowers. There is every reason to believe the same model can continue to develop in New Zealand.

International lessons for New Zealand

The experience of the United States, Europe, and Australia offers several important lessons.

-

First, private credit does not replace banks. It complements them.

-

Second, successful private credit markets are built on disciplined underwriting, strong governance, and long-term relationships.

-

Third, businesses benefit when multiple sources of capital are available.

The most resilient economies are those where businesses can access capital from a variety of providers rather than relying on a single source. New Zealand has an opportunity to continue building precisely that type of ecosystem. That is the opportunity in front of us.

Looking ahead

New Zealand has no shortage of quality businesses. What it has historically lacked is a sufficient diversity of capital providers. Private credit is helping address that challenge. The opportunity is not to replace banks. The opportunity is not to lower credit standards. The opportunity is to create a broader, more resilient capital ecosystem that combines the strengths of banks, institutional investors, and private credit providers to support the next generation of New Zealand businesses.

Having spent much of my career in banking before moving into private credit, I do not view the future as banks versus private credit. I view it as banks and private credit working together to provide New Zealand businesses with a broader range of funding solutions. The businesses that will drive New Zealand's next phase of growth deserve access to both.

TJ Singh is Principal – Private Credit at Harbour Asset Management. This content is supplied free to NBR. It is not intended as financial advice.

Disclosure of interest: Harbour Asset Management is the investment manager for portfolios that invest into companies and asset classes mentioned in this article.

* Financing the Economy - 2025

** Infometrics Regional Economic Profile 2025

IMPORTANT NOTICE AND DISCLAIMER

This publication is provided for general information purposes only. The information provided is not intended to be financial advice. The information provided is given in good faith and has been prepared from sources believed to be accurate and complete as at the date of issue, but such information may be subject to change. Past performance is not indicative of future results and no representation is made regarding future performance of the Funds. No person guarantees the performance of any funds managed by Harbour Asset Management Limited.

Harbour Asset Management Limited (Harbour) is the issuer of the Harbour Investment Funds. A copy of the Product Disclosure Statement is available at https://www.harbourasset.co.nz/our-funds/investor-documents/. Harbour is also the issuer of Hunter Investment Funds (Hunter). A copy of the relevant Product Disclosure Statement is available at https://hunterinvestments.co.nz/resources/. Please find our quarterly Fund updates, which contain returns and total fees during the previous year on those Harbour and Hunter websites. Harbour also manages wholesale unit trusts. To invest as a wholesale investor, investors must fit the criteria as set out in the Financial Markets Conduct Act 2013.