2025 shaped up to be a much better year for the Chinese economy than what financial analysts thought possible. The shock of Liberation Day and subsequent tariffs escalation weighed heavily on economic forecasts for China. Yet, as it turned out, tariffs became less punitive and China showed a remarkable ability to export into new and growing markets to more than make up for lost exports to the U.S.

Source: Bloomberg

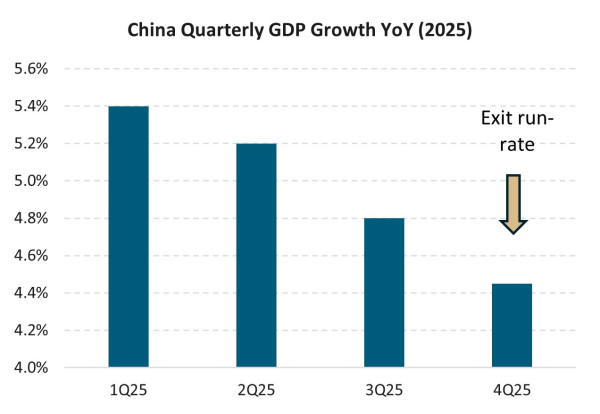

However, growth momentum slowed during the year, and the December quarter was the weakest of the year. Hence, the market is debating what 2026 might look like, and as New Zealand’s largest trading partner, our economic future is fundamentally linked to China’s economic performance.

Source: Bloomberg

Dairy, meat, logs, and fruit are the key goods exports, while tourism, education, and transportation are key services exports. From China, we import items like machinery and electrical equipment, furniture, and vehicles. Listed companies trading on the NZX, such as Fonterra, a2 Milk, and Scales have direct exposure to the Chinese consumer, and being on the right side of Chinese economic forces can be helpful for asset prices and local company profits.

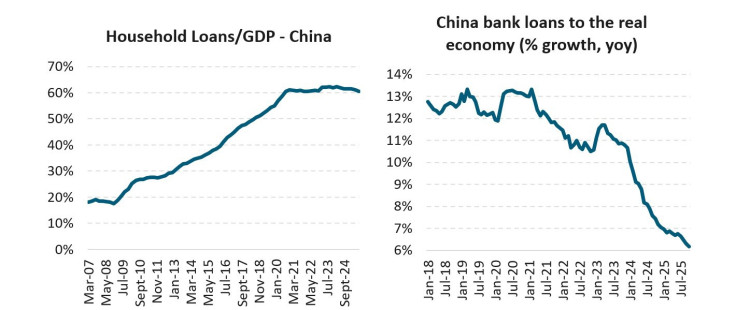

It is remarkably easy to find data to fit anyone’s confirmation bias on China, and we have seen the sustained downturn in the property market spread into low consumer sentiment and retail spending. Chinese policymakers have launched many initiatives to smooth the consumption cycle, yet increased household savings, anaemic credit growth to the real economy, and a declining population are favourite talking points among analysts.

Source: Bloomberg

Yet we are inclined to take a half-glass-full approach to the Chinese growth outlook. Whilst we await the details of the new five-year-plan to see the strategic policy direction, it seems clear to us that China has, through a deliberate and focused policy agenda, engineered a strong base to grow new industries, like new energy (including solar, batteries and electric cars), artificial intelligence, robotics and other high-tech sectors. Looking at old and trusted indicators of property development and roading infrastructure no longer suffices in telling the story of Chinese growth.

The GDP growth target for 2026 has not yet been set, and should be published in early March, during the National People’s Congress (NPC). The new target is expected to be in the 4.5% to 5% range (was ‘around 5%’ in 2025). Whatever the target is, it gives a pretty good indication of where growth is heading and the amount of stimulus that might be needed to get there. With geopolitical uncertainties still very much a risk to growth rates, it is reasonable to think policymakers will retain some dry powder until the second half of the year in the event they find themselves trailing the target.

Consumers are likely to remain cautious as they continue to adjust spending in line with property values and employment prospects. However, the over 20% return on Chinese shares in the last 12 months and improved sentiment in Chinese technological strength (with the launch of DeepSeek being the watershed moment) are likely to help offset worries linked to property and labour markets and could see spending return to more normal growth rates.

In the meantime, we are selectively investing in iron ore and copper companies with diversified exposures to the growing Chinese new energy sector, but with balanced exposures to the rest of the world, which is also investing heavily in AI and data centre infrastructure hungry for industrial metals. Similarly, we are being very targeted in the exposure to Chinese consumers, focusing on horticultural investments where the Chinese consumer has an appreciation for high-quality New Zealand-grown fruits.

Our largest exposure, however, is to the infant formula market and a2 Milk. This is, of course, a position that is carefully considered as part of a diversified portfolio of other assets (and should not in any form be considered financial advice), and subject to change should the investment thesis change. However, after a very soft 2025 birth-rate in China, it is reasonable to wonder why an investment in infant formula is ok. Part of our thesis is sustained market share gains with plenty of available share-gains still available; vertical integration of manufacturing to enable faster product innovation and margin capture; and exceptional strategic and operational management.

As New Zealand investors, keeping a watching-brief on the Chinese economy is prudent given its wide-spread impact on our own economy and companies. Right now, our view is that momentum is positive, despite a meaningful slowdown in GDP growth towards the end of 2025. Our direct exposures via commodities and services have a gentle bid-tone that is benefitting especially the New Zealand agricultural sector and the Australian metals and mining sector.

At Harbour, we carefully monitor both Chinese domestic policy initiatives – with the upcoming NPC conference as a near-term springboard for possible new project announcements – and geopolitical developments that have proven to be more unpredictable and potentially disruptive for asset pricing and investment returns. Views can change quickly in this context, however we are constructive on China’s ability to navigate choppy seas having seen the super-charging of exports last year.

IMPORTANT NOTICE AND DISCLAIMER

This publication is provided for general information purposes only. The information provided is not intended to be financial advice. The information provided is given in good faith and has been prepared from sources believed to be accurate and complete as at the date of issue, but such information may be subject to change. Past performance is not indicative of future results and no representation is made regarding future performance of the Funds. No person guarantees the performance of any funds managed by Harbour Asset Management Limited.

Harbour Asset Management Limited (Harbour) is the issuer of the Harbour Investment Funds. A copy of the Product Disclosure Statement is available at https://www.harbourasset.co.nz/our-funds/investor-documents/. Harbour is also the issuer of Hunter Investment Funds (Hunter). A copy of the relevant Product Disclosure Statement is available at https://hunterinvestments.co.nz/resources/. Please find our quarterly Fund updates, which contain returns and total fees during the previous year on those Harbour and Hunter websites. Harbour also manages wholesale unit trusts. To invest as a wholesale investor, investors must fit the criteria as set out in the Financial Markets Conduct Act 2013.