- The biotech sector, both private and public, has a plethora of new drugs and treatments in the pipeline courtesy of large capital injections 5–7 years ago.

- However, there needs to be another capital infusion to bring these opportunities to market. The key question is who will fund these opportunities and who will capture the anticipated returns.

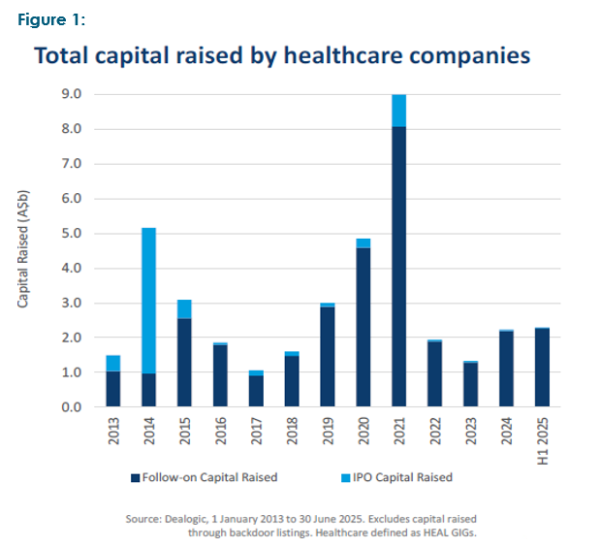

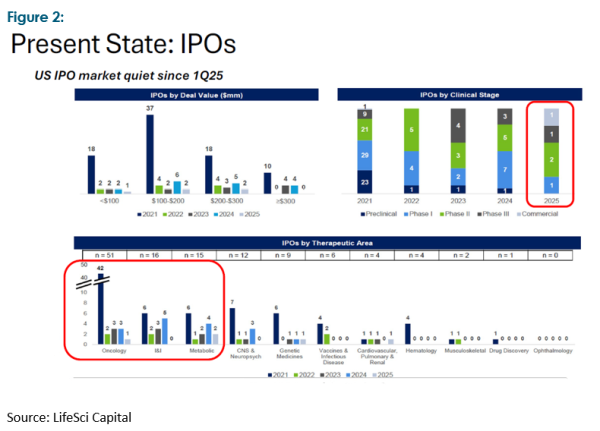

We recently attended an Australasian biotech conference that featured over forty biotech companies ranging from pre-clinical through to early commercialisation. The companies’ activities spanned the breadth of the sector but there was one single common feature: a need for additional capital to see them through to commercialisation. The guest speaker neatly summed up the situation by observing that five to seven years ago the sector was “hot” and awash with money, as evidenced in Figures 1 and 2.

This has seen a raft of new and often novel drugs and therapies emerge from universities and other scientific institutions, many of which are now approaching the most expensive stage of medical development, phase 3 studies and/or proving up commercial viability. Phase 3 studies can range from US$30 million to over $500 million, and generally take 2–3 years to complete, though this timeframe may vary considerably depending on numerous factors.

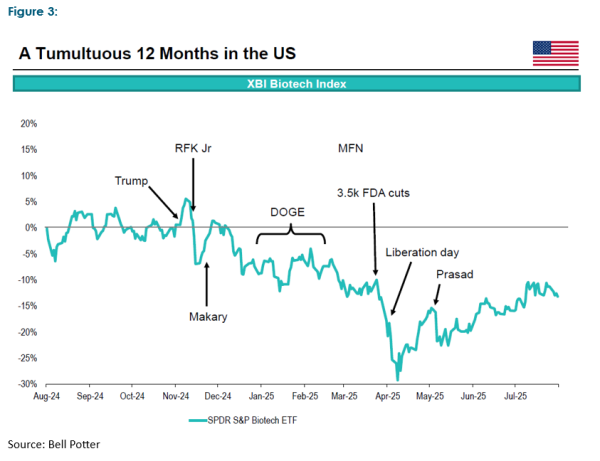

In Australia alone, there are over 165 listed healthcare companies, the majority of which have market values under $100m and have yet to develop a commercial business case. However, global public markets have seen the healthcare sector fall from favour in recent times, not helped by the turmoil currently inflicted on the US healthcare industry by the new political administration.

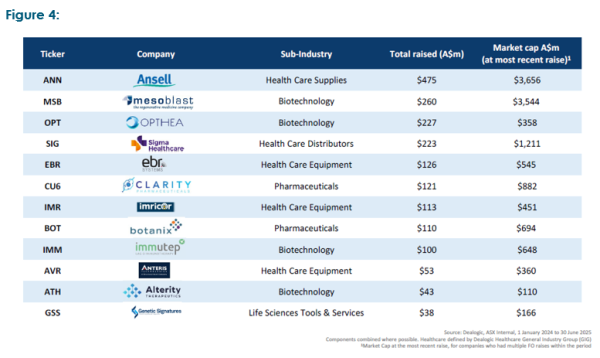

Despite the underwhelming performance of the listed healthcare sector, capital markets have remained open to funding activity. Figure 4 highlights raisings over the last twelve months in Australia (and, more recently, radio pharmaceutical company Clarity raised a further $203m in July this year). Nevertheless, given the appetite for capital displayed at the conference and the risks associated with many of the propositions, it is highly unlikely public capital markets alone have the necessary capacity to meet all these capital needs. Earlier stage propositions are attracting private wealth and venture capital players. However, they are unlikely to fund all the studies requiring phase 3 trials and beyond. Government funding via grants and other assistance is also helping to bridge the funding gap in some instances.

There have been several players (including Telix, Neuren, Mesoblast, Botanix, and EBR Systems) who have managed to break through into commercial territory despite this funding hurdle, providing a slightly more mature cohort of investable biotech companies. However, this path is rarely a smooth one, and success is far from guaranteed (witness Opthea and Percheron).

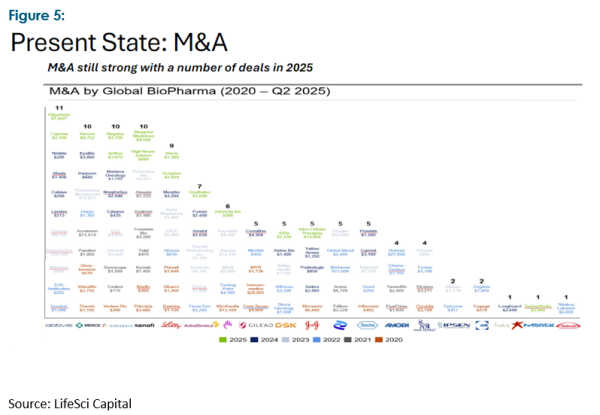

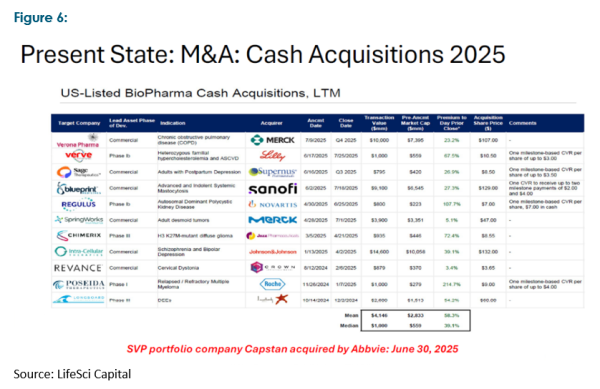

Fortunately, as we noted in an earlier Harbour Navigator, the biotech industry is an attractive hunting ground for the big global pharma companies. As Figures 5 and 6 show, big pharma has been active over the last five years, and their acquisition appetite has not faltered in the last six months.

The “problem” with selling out to big pharma is the perceived transfer of value. Neuren’s CEO is on record as saying the need to secure a commercial partner for its first-generation drug, Daybue, saw them “pay away”, in his opinion, over two thirds of its underlying value. However, having secured a much stronger financial footing because of this transaction, the company intends to take its second-generation drug (NNZ-2591) through at least two phase 3 studies and capture much more of the value upside (assuming the drug performs as expected!). This perception is consistent with most presenters at the conference, who recognised getting through to at least a robust phase 2B study effectively de-risks their proposals and translates into a much better payback.

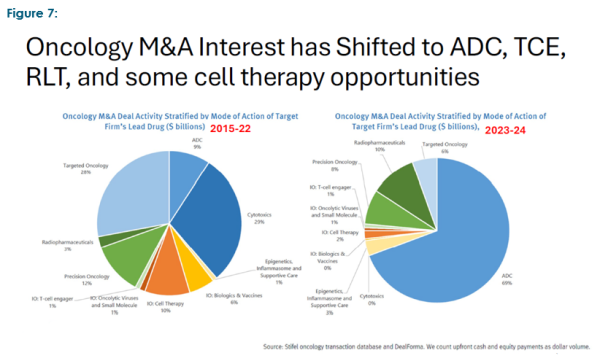

Outside the capital demands the sector is experiencing, there are two other key observations we wish to highlight: first, while the conference presented a wide range of drug, therapy and medical device companies, M&A focus has moved to several key areas targeting unmet needs (which arguably have an easier time getting through regulatory hurdles) such as ADC’s (anti-body drug conjugates, i.e. cancer drugs that combine targeted therapy with chemotherapy), TCE (T-cell engagers), RLT’s (radioligand therapeutics) and cell therapies. There has also been a move towards precision, targeted, and platform approaches (particularly in gene and cell therapy), and where possible a desire to secure FDA regulatory fast track approvals.

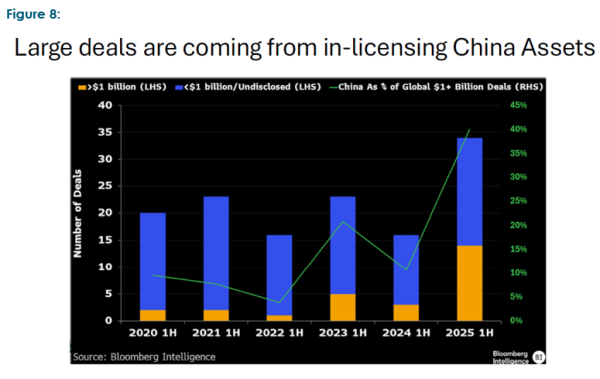

The second area was the references to China made by various presenters. While the US remains the blue-chip gateway to commercial success, both in regard to regulatory approvals and attractive end markets, China has prioritised the biotech sector, providing both capital and a favorable regulatory setting over the last ten years. It is increasingly becoming a source of interesting intellectual capital and end market. Figure 8 illustrates this trend.

In summary, there is a flood of potential new drugs and therapies emerging. Although, how many achieve commercialisation will be dictated by a combination of both clinical success and capital backing. The cost of bringing new solutions to market is formidable and the risk of failure for many of these novel new treatments is not insignificant. Despite this potential funding roadblock, there is a raft of exciting new treatments that promise to address many of the problems facing the healthcare sector today.

IMPORTANT NOTICE AND DISCLAIMER

This publication is provided for general information purposes only. The information provided is not intended to be financial advice. The information provided is given in good faith and has been prepared from sources believed to be accurate and complete as at the date of issue, but such information may be subject to change. Past performance is not indicative of future results and no representation is made regarding future performance of the Funds. No person guarantees the performance of any funds managed by Harbour Asset Management Limited.

Harbour Asset Management Limited (Harbour) is the issuer of the Harbour Investment Funds. A copy of the Product Disclosure Statement is available at https://www.harbourasset.co.nz/our-funds/investor-documents/. Harbour is also the issuer of Hunter Investment Funds (Hunter). A copy of the relevant Product Disclosure Statement is available at https://hunterinvestments.co.nz/resources/. Please find our quarterly Fund updates, which contain returns and total fees during the previous year on those Harbour and Hunter websites. Harbour also manages wholesale unit trusts. To invest as a wholesale investor, investors must fit the criteria as set out in the Financial Markets Conduct Act 2013.