The latest oil shock is reinforcing electrification and energy security trends already underway, not resetting the system.

The conflict in the Middle East has triggered a renewed and significant oil price shock, resurfacing familiar concerns around energy security, fuel affordability and exposure to geopolitically fragile supply chains. However, unlike previous oil shocks, this episode is unfolding at a time when global energy systems are already undergoing rapid change.

While oil market disruptions are not new, this shock is occurring against a markedly different energy backdrop - one where climate constraints, rising electricity demand and prior policy action have already accelerated electrification and large-scale renewable investment.

For investors, the key question is whether this shock marks a new structural shift in global energy systems, simply accelerates trends already in motion, or proves to be a temporary disruption that fades as geopolitical tensions ease.

From an investment perspective, this distinction matters. Structural change reshapes long term asset values, capital allocation and risk premia; temporary shocks mainly influence short-term volatility.

Acceleration, by contrast, occurs when shocks reinforce existing policy objectives, pull forward investment already underway, and increase adoption of technologies that are already competitive.

Evidence points to acceleration not a systemic reset

Electrification trends were already well entrenched prior to the current conflict. Globally, renewable development pipelines now span hundreds of gigawatts across multiple countries/regions including China, Europe, Australia, New Zealand and the United States.

Policy responses to the current oil shock have largely reinforced existing energy strategies rather than introduced fundamentally new frameworks.

China’s response to energy supply shocks in the early 2000s led to sustained efforts to expand domestic generation and diversify supply - dynamics that continue to shape its energy system today. By the first quarter of 2025, China’s operating wind and solar capacity reached approximately 1.4 terawatts, surpassing thermal power for the first time and meeting incremental electricity demand growth, this capacity would comfortably meet the generation needs of Japan. While momentum in renewable energy development in China may be slowing, China’s pipeline also exceeds one terawatt.

In Europe, the transition is similarly advanced, driven by Europe’s commitments under the Paris agreement and the existing Russia-Ukraine conflict already raising concerns for energy security within Europe, renewable sources now account for approximately 47% of electricity generation.

France has recently announced a doubling of state support to switch from oil and gas to electricity. The United Kingdom’s 2023 Energy Act has seen the announcement of GBP 40 billion of annual investment in renewable energy to drive progress toward their 2030 clean power target. In the United States, more than 180 GW of utility‑scale renewable energy capacity is currently in the development pipeline.

New Zealand benefits from a relatively high share of renewable electricity generation, shaped in part by its response to energy shocks in the 1970s. The economic disruption of the period contributed to large‑scale state‑led initiatives, including the “Think Big” projects of the 1980s, aimed at reducing vulnerability to external energy shocks.

New Zealand companies appear relatively well positioned. As at August 2025, the pipeline comprised 289 generation projects with a combined planned capacity of 44.29 gigawatts, approximately 82 percent of which is intermittent renewable generation, primarily solar and wind. Battery installations that will support firming also surged in 2025, with the total capacity installed across the year — 1.9 GW (4.9 GWh), outpacing the combined figure for the previous eight years.

This pipeline is more than four times current installed national capacity, indicating that much of the transition groundwork is already in place. The Driving Sustainable Growth: Opportunities for New Zealand’s Economy paper highlights how early investment in electrification and clean energy can improve competitiveness, resilience and cost stability - benefits that are reinforced rather than created by the current oil shock.

Not all events that have reshaped climate policy relate to energy. The devastating Australian bushfires marked a political and policy inflection point, accelerating the adoption of more ambitious climate and energy targets following the 2022 federal election. Australia has maintained strong renewable capacity additions alongside a record surge in utility‑scale battery installations, supporting system reliability rather than fuel substitution.

Could demand side behaviour change the picture?

What could point to a more durable structural shift is the potential changes in consumer and demand side behaviour. Electric vehicle sales jumped significantly in the March quarter across the United Kingdom, United States, Australia and New Zealand with United Kingdom electric car sales rising to their highest ever level in March. Rooftop solar, battery storage deployment and heavy transport electrification are accelerating, while sustainable aviation fuel development continues to expand.

Electrification offers benefits across security, affordability and supply reliability, and is increasingly competitive with fossil fuels. It is far too early to tell how long the increased demand for electric transportation and renewable energy options will last but with improving technology and reducing costs, the economics are competitive with fossil fuel alternatives, even without the current price volatility.

Investor Implications

A recent Bloomberg energy review noted that global investment in the energy transition reached US$2.3 trillion in 2025 outpacing fossil fuel investment for a second consecutive year. Investments in renewable energy, grid investment and electrified transport receiving the largest allocation. Bloomberg suggest that average annual investment in renewable energy will reach US$2.9 trillion in the next five years. Strong policy support, falling technology costs, and growing corporate climate commitments already in place prior to the Middle East conflict has already positioned renewables as a dominant force in the global energy transition. Governments increasingly view renewable energy as a means of delivering affordable power while strengthening long‑term energy security. For investors, exposure to renewable infrastructure, storage technologies, and distributed energy solutions offers long-duration cash flows, and in some cases, inflation-linked returns.

Investment returns remain driven by company‑specific fundamentals, valuation discipline and market structure, making it overly simplistic to frame renewables versus fossil fuels as a binary choice.

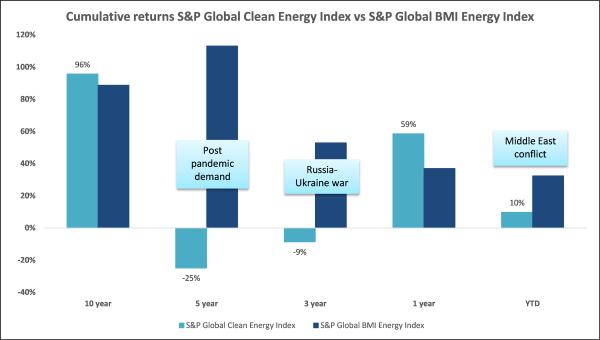

Taking a macro market view, the chart below compares the cumulative returns of listed renewable energy companies with listed oil and gas companies over the past decade. While oil and gas companies have experienced periods of outperformance, renewable energy companies have marginally outperformed over the full ten-year period. We would be surprised to see this current period of outperformance for oil and gas companies continue in the medium to long term.

While the path has been volatile, clean energy's convergence on long-run returns make a compelling case for the energy transition - and supports the case that the transition was already well under way before the current energy shock.

Source: Bloomberg / Harbour Asset Management

History shows that only a subset of energy shocks lead to lasting structural change. Based on the available evidence, the current Middle East conflict appears more likely to accelerate trends already in motion - particularly electrification and renewable deployment - than to reset the energy system. While near-term volatility may be significant, the more durable signal lies in how governments, firms and investors respond, and much of that response was already underway.

Sue Walker is Senior Manager, Responsible Investment at Harbour Asset Management. This content is supplied free to NBR. It is not intended as financial advice.

Disclosure of interest: Harbour Asset Management is the investment manager for portfolios that invest into companies and asset classes mentioned in this article.

IMPORTANT NOTICE AND DISCLAIMER

This publication is provided for general information purposes only. The information provided is not intended to be financial advice. The information provided is given in good faith and has been prepared from sources believed to be accurate and complete as at the date of issue, but such information may be subject to change. Past performance is not indicative of future results and no representation is made regarding future performance of the Funds. No person guarantees the performance of any funds managed by Harbour Asset Management Limited.

Harbour Asset Management Limited (Harbour) is the issuer of the Harbour Investment Funds. A copy of the Product Disclosure Statement is available at https://www.harbourasset.co.nz/our-funds/investor-documents/. Harbour is also the issuer of Hunter Investment Funds (Hunter). A copy of the relevant Product Disclosure Statement is available at https://hunterinvestments.co.nz/resources/. Please find our quarterly Fund updates, which contain returns and total fees during the previous year on those Harbour and Hunter websites. Harbour also manages wholesale unit trusts. To invest as a wholesale investor, investors must fit the criteria as set out in the Financial Markets Conduct Act 2013.